Band 1

Neu

Bitte laden Sie die Seite neu und versuchen es noch einmal.

Bitte laden Sie die Seite neu und versuchen es noch einmal.

Bitte laden Sie die Seite neu und versuchen es noch einmal.

Sie helfen uns damit, unseren Shop zu verbessern.

15%** auf Schreibwaren und Kalender!

Schockierend, dark und sexy!

Das furiose Finale der Cornwall-Reihe!

S.T. Abby

Secret – Du sollst mich fürchtenBuch (Taschenbuch)

12,00 €

Peter Wachendorf

Lies mal - Hefte Band 1 und Band 2 (Paket)Schulbuch (Set mit diversen Artikeln)

5,60 €

Diercke Weltatlas - Ausgabe 2023

Schulbuch (Set mit diversen Artikeln)

36,50 €

Peter Wachendorf

Lies mal - Die Hefte Band 1 und Band 2 im Paket (Ente und Frosch)Schulbuch (Set mit diversen Artikeln)

5,60 €

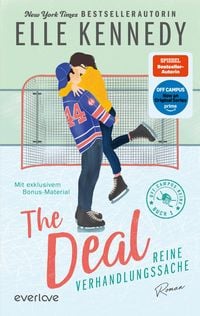

Elle Kennedy

The Deal – Reine VerhandlungssacheBuch (Taschenbuch)

15,00 €

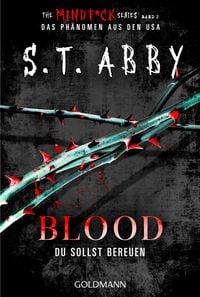

S.T. Abby

Blood – Du sollst bereuenBuch (Taschenbuch)

12,00 €

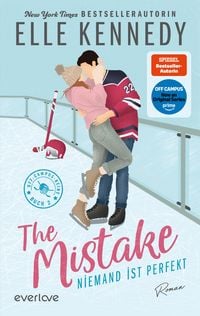

Elle Kennedy

The Mistake – Niemand ist perfektBuch (Taschenbuch)

15,00 €

Flex und Flo - Ausgabe 2021

Schulbuch (Paperback)

24,95 €

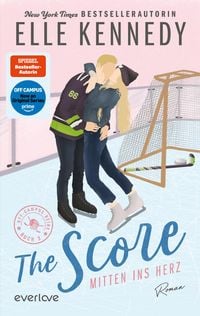

Elle Kennedy

The Score – Mitten ins HerzBuch (Taschenbuch)

15,00 €

Peter Wachendorf

Lies mal - Das Heft mit dem KükenSchulbuch (Geheftet)

3,90 €

Denken und Rechnen - Allgemeine Ausgabe 2024

Schulbuch (Set mit diversen Artikeln)

22,95 €

Wanna be my Lover mit exklusivem Farbschnitt

Buch

18,00 €

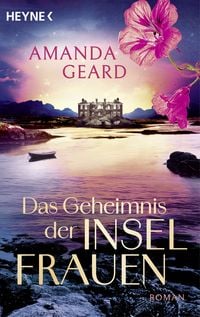

Amanda Geard

Das Geheimnis der InselfrauenBuch (Taschenbuch)

14,00 €

Titus Müller

Die geheime MissionBuch (Taschenbuch)

17,00 €

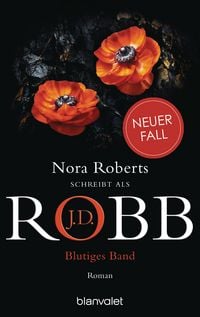

J.D. Robb

Blutiges BandBuch (Taschenbuch)

13,00 €

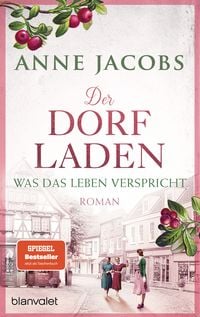

Anne Jacobs

Der Dorfladen - Was das Leben versprichtBuch (Taschenbuch)

12,00 €

Jo Nesbo

Insel der RattenBuch (Gebundene Ausgabe)

19,99 €

David Safier

00-LaschetBuch (Taschenbuch)

18,00 €

Leanne Shapton, Gabriele von Arnim, Lin Hierse, Jovana Reisinger + weitere

Die DamentoiletteBuch (Gebundene Ausgabe)

20,00 €

S.T. Abby

Secret – Du sollst mich fürchtenBuch (Taschenbuch)

12,00 €

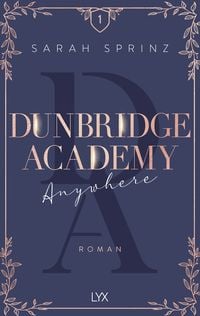

Sarah Sprinz

Dunbridge Academy - WhoeverBuch (Taschenbuch)

16,90 €

Lucy Astner

Kein Sommer ohne AugustBuch (Taschenbuch)

16,00 €

Rina Kent

Reign of a KingBuch (Taschenbuch)

19,00 €

Virginia Evans

Die BriefeschreiberinBuch (Taschenbuch)

14,00 €

Rebecca Yarros

Untitled Empyrean (Not Book Four)Buch (Gebundene Ausgabe)

27,99 €

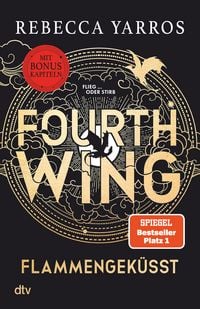

Rebecca Yarros

Flammengeküsst – Ohne Titel (nicht Band 4)Buch (Gebundene Ausgabe)

28,00 €

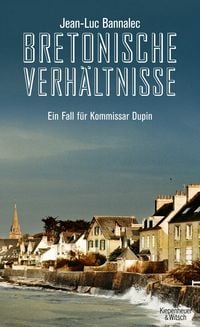

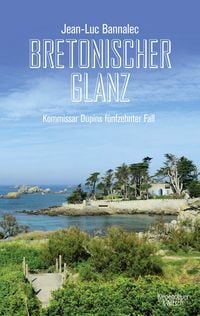

Jean-Luc Bannalec

Bretonischer GlanzBuch (Taschenbuch)

18,00 €

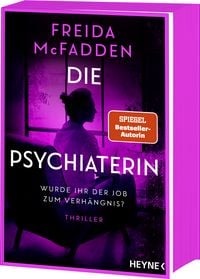

Freida McFadden

Die Psychiaterin – Wurde ihr der Job zum Verhängnis?Buch (Taschenbuch)

17,00 €

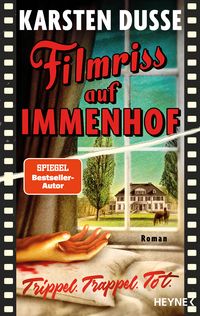

Karsten Dusse

Filmriss auf ImmenhofBuch (Gebundene Ausgabe)

24,00 €

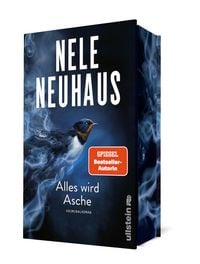

Nele Neuhaus

Alles wird AscheBuch (Gebundene Ausgabe)

26,00 €

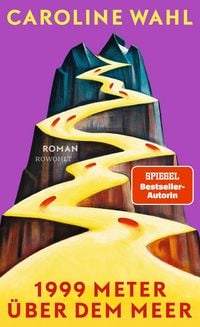

Caroline Wahl

1999 Meter über dem MeerBuch (Gebundene Ausgabe)

24,00 €

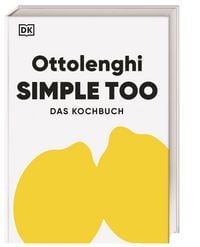

Yotam Ottolenghi + weitere

Ottolenghi Simple tooBuch (Gebundene Ausgabe)

40,00 €

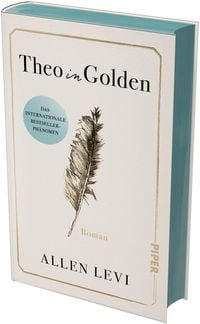

Allen Levi

Theo in GoldenBuch (Gebundene Ausgabe)

26,00 €

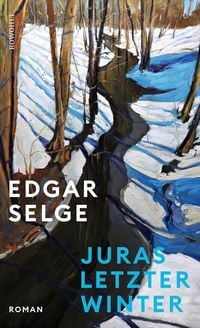

Edgar Selge

Juras letzter WinterBuch (Gebundene Ausgabe)

25,00 €

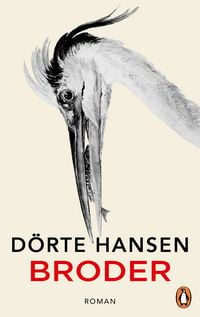

Dörte Hansen

BroderBuch (Gebundene Ausgabe)

26,00 €

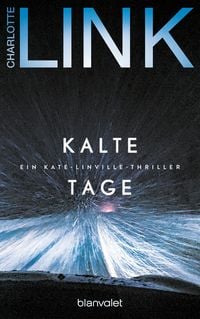

Charlotte Link

Kalte TageBuch (Gebundene Ausgabe)

26,00 €

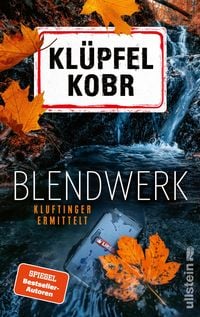

Volker Klüpfel + weitere

BlendwerkBuch (Gebundene Ausgabe)

25,00 €

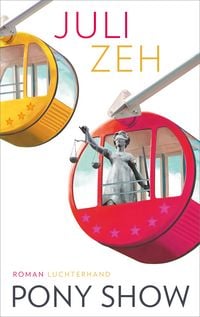

Juli Zeh

Pony ShowBuch (Gebundene Ausgabe)

25,00 €

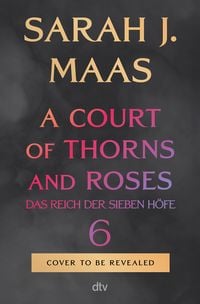

Sarah J. Maas

A Court of Thorns and Roses 6Buch (Gebundene Ausgabe)

30,00 €

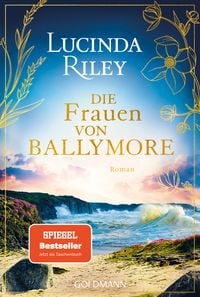

Lucinda Riley

Die Frauen von BallymoreBuch (Taschenbuch)

13,00 €

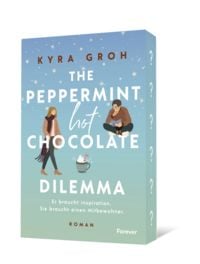

Kyra Groh

The Peppermint Hot Chocolate DilemmaBuch (Taschenbuch)

16,99 €

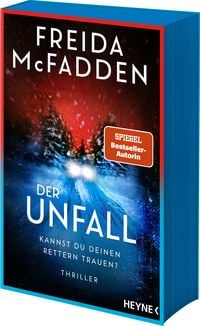

Freida McFadden

Der Unfall – Kannst du deinen Rettern trauen?Buch (Taschenbuch)

17,00 €

Hera Lind

Erhobenen HauptesBuch (Taschenbuch)

13,00 €

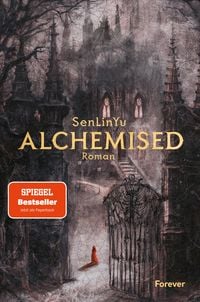

SenLinYu

AlchemisedBuch (Taschenbuch)

20,00 €

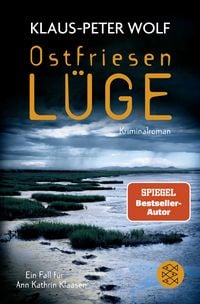

Klaus-Peter Wolf

OstfriesenlügeBuch (Taschenbuch)

14,00 €

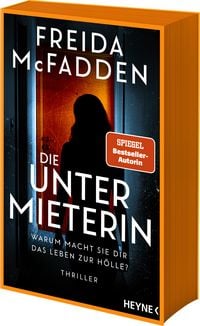

Freida McFadden

Die Untermieterin – Warum macht sie dir das Leben zur Hölle?Buch (Taschenbuch)

17,00 €

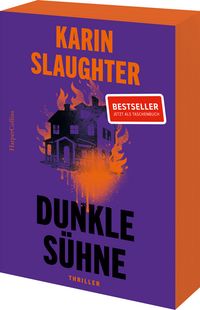

Karin Slaughter

Dunkle SühneBuch (Taschenbuch)

14,00 €

Sebastian Fitzek

AmokspielBuch (Gebundene Ausgabe)

25,00 €

Carsten Henn

Schascha und der BuchspaziererBuch (Gebundene Ausgabe)

18,00 €

Stefanie Sargnagel

OktoberfestBuch (Gebundene Ausgabe)

18,00 €

Sonja Sophie Kreis

Das große EisBuch (Gebundene Ausgabe)

24,00 €

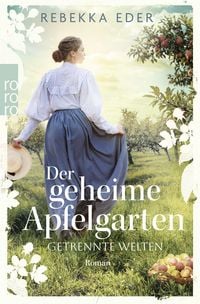

Rebekka Eder

Der geheime Apfelgarten: Getrennte WeltenBuch (Taschenbuch)

14,00 €

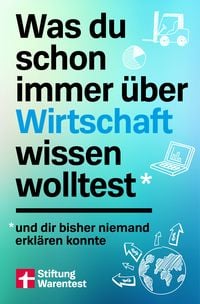

Olaf Wittrock

Was du schon immer über Wirtschaft wissen wolltestBuch (Taschenbuch)

16,90 €

Christian Heinrich

15 Entscheidungen, die dein Leben verlängernBuch (Taschenbuch)

16,90 €

Nele Neuhaus

Alles wird AscheBuch (Gebundene Ausgabe)

26,00 €

Caroline Wahl

1999 Meter über dem MeerBuch (Gebundene Ausgabe)

24,00 €

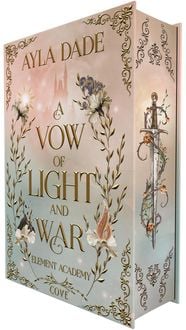

Ayla Dade

A Vow of Light and War (Element Academy 1)Buch (Gebundene Ausgabe)

26,00 €

Yotam Ottolenghi + weitere

Ottolenghi Simple tooBuch (Gebundene Ausgabe)

40,00 €

Allen Levi

Theo in GoldenBuch (Gebundene Ausgabe)

26,00 €

Edgar Selge

Juras letzter WinterBuch (Gebundene Ausgabe)

25,00 €

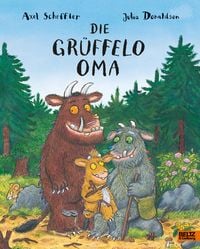

Axel Scheffler + weitere

Die Grüffelo-OmaBuch (Gebundene Ausgabe)

16,00 €

Rebecca Yarros

Untitled Empyrean (Not Book Four)Buch (Gebundene Ausgabe)

27,99 €

Charlotte Link

Kalte TageBuch (Gebundene Ausgabe)

26,00 €

Carsten Herbert

Einfach sanierenBuch (Taschenbuch)

24,90 €

Beate Backhaus + weitere

Vererben und ErbenBuch (Taschenbuch)

29,90 €

Werner Siepe

Mein gutes Recht als VerbraucherBuch (Taschenbuch)

16,90 €

Volker Klüpfel + weitere

BlendwerkBuch (Gebundene Ausgabe)

25,00 €

Linus Geschke

Die SchluchtBuch (Taschenbuch)

17,00 €

Clara Lösel

Ich dachte, sowas fühl nur ichBuch (Gebundene Ausgabe)

20,00 €

Mareike Fallwickl

Haltet euch festBuch (Gebundene Ausgabe)

24,00 €

Romy Fölck

Die RegenschwimmerinBuch (Gebundene Ausgabe)

24,00 €

Juli Zeh

Pony ShowBuch (Gebundene Ausgabe)

25,00 €

Sarah J. Maas

A Court of Thorns and Roses 6Buch (Gebundene Ausgabe)

30,00 €

Lucinda Riley

Die Frauen von BallymoreBuch (Taschenbuch)

13,00 €

Kyra Groh

The Peppermint Hot Chocolate DilemmaBuch (Taschenbuch)

16,99 €

Freida McFadden

Der Unfall – Kannst du deinen Rettern trauen?Buch (Taschenbuch)

17,00 €

Hera Lind

Erhobenen HauptesBuch (Taschenbuch)

13,00 €

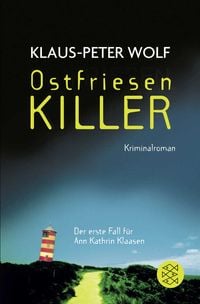

Klaus-Peter Wolf

OstfriesenlügeBuch (Taschenbuch)

14,00 €

Freida McFadden

Die Untermieterin – Warum macht sie dir das Leben zur Hölle?Buch (Taschenbuch)

17,00 €

Dani Francis

Broken DoveBuch (Gebundene Ausgabe)

24,00 €

Matt Dinniman

Carl's Doomsday ScenarioBuch (Taschenbuch)

18,00 €

Louisa Dellert

UnshameBuch (Taschenbuch)

18,99 €

Marah Woolf

Falling AsgardBuch (Gebundene Ausgabe)

24,00 €

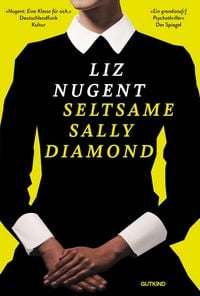

Liz Nugent

Seltsame Sally DiamondBuch (Taschenbuch)

16,00 €

Sophia Como

HalbwachBuch (Taschenbuch)

17,00 €

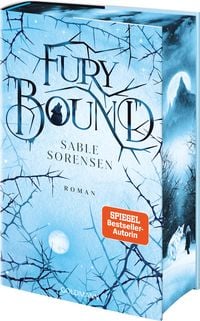

Sable Sorensen

Fury BoundBuch (Gebundene Ausgabe)

25,00 €

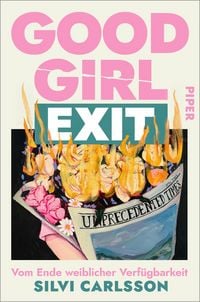

Silvi Carlsson

Good Girl ExitBuch (Taschenbuch)

18,00 €

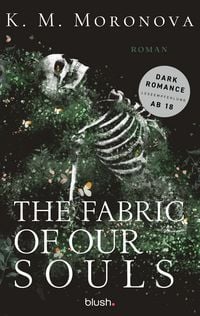

K. M. Moronova

The Fabric of Our SoulsBuch (Taschenbuch)

17,00 €

Anna Lane

Mornings in Boston - The Games We PlayBuch (Taschenbuch)

16,90 €

Elle Kennedy

Love SongBuch (Taschenbuch)

16,00 €

H.D. Carlton

PhantomBuch (Taschenbuch)

19,00 €

April Dawson

Building TrustBuch (Taschenbuch)

16,90 €

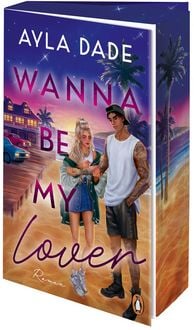

Ayla Dade

Wanna be my loverBuch (Taschenbuch)

18,00 €

Damian Richter

Dein Neustart beginnt jetztBuch (Taschenbuch)

20,00 €

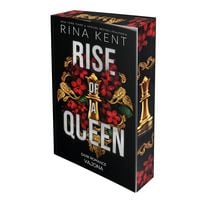

Rina Kent

Rise of a QueenBuch (Taschenbuch)

19,00 €

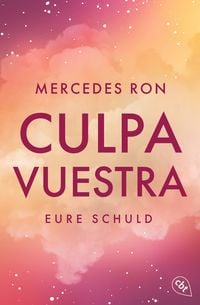

Mercedes Ron

Culpa Vuestra – Eure SchuldBuch (Taschenbuch)

16,00 €

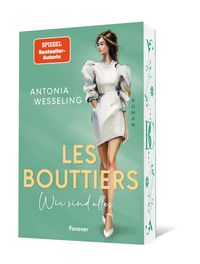

Antonia Wesseling

Les Bouttiers – Wir sind allesBuch (Taschenbuch)

16,99 €

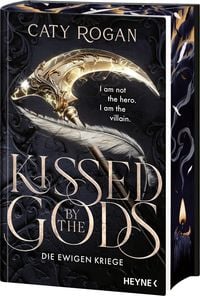

Caty Rogan

Kissed by the Gods – Die ewigen KriegeBuch (Gebundene Ausgabe)

25,00 €

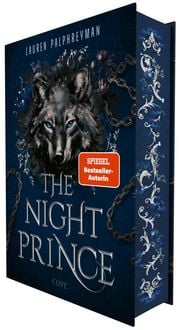

Lauren Palphreyman

The Night Prince (Wolf King 2)Buch (Gebundene Ausgabe)

25,00 €

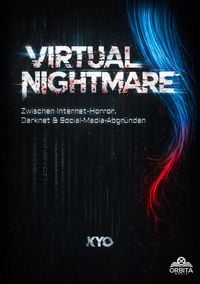

Kyo

Virtual NightmareBuch (Taschenbuch)

19,99 €

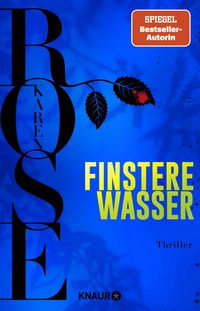

Karen Rose

Finstere WasserBuch (Taschenbuch)

19,99 €

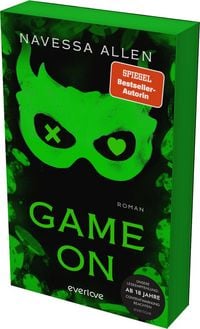

Navessa Allen

Game onBuch (Taschenbuch)

17,00 €

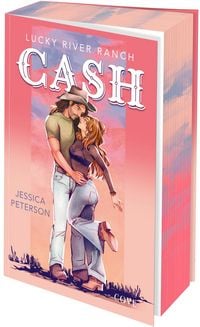

Jessica Peterson

Cash (Lucky River Ranch 1)Buch (Taschenbuch)

17,00 €

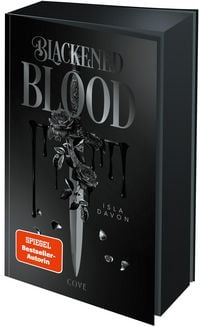

Isla Davon

Blackened Blood (Blackened Blade 3)Buch (Taschenbuch)

19,00 €

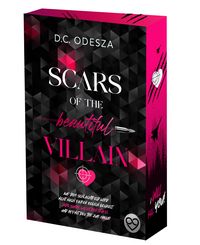

D.C. Odesza

SCARS of the beautiful VILLAINBuch (Taschenbuch)

18,90 €

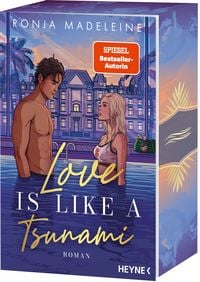

Ronja Madeleine

Love is like a TsunamiBuch (Taschenbuch)

17,00 €

Rachel Gillig

One Dark Window: Special EditionBuch (Gebundene Ausgabe)

26,00 €

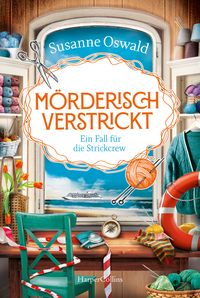

Susanne Oswald

Mörderisch verstrickt – Ein Fall für die StrickcrewBuch (Taschenbuch)

13,00 €

Brittainy Cherry

Wie das Schweigen vor der FlutBuch (Taschenbuch)

16,00 €

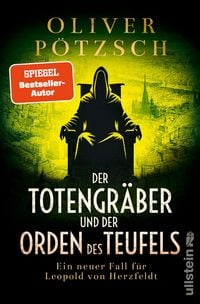

Oliver Pötzsch

Der Totengräber und der Orden des TeufelsBuch (Taschenbuch)

17,99 €

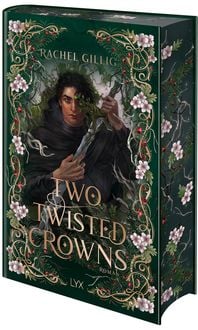

Rachel Gillig

Two Twisted Crowns: Special EditionBuch (Gebundene Ausgabe)

26,00 €

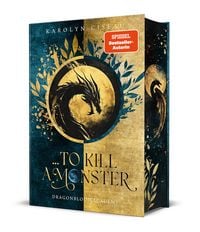

Karolyn Ciseau

… to Kill a Monster. Dragonblood AcademyBuch (Gebundene Ausgabe)

25,00 €

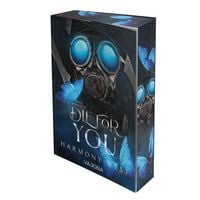

Harmony West

Die for YouBuch (Taschenbuch)

18,00 €

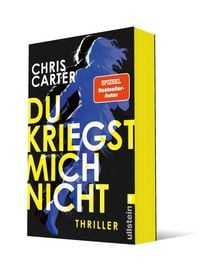

Chris Carter

Du kriegst mich nichtBuch (Taschenbuch)

18,00 €

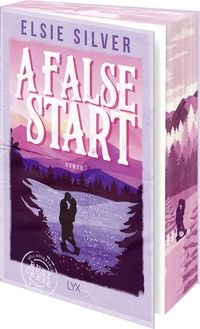

Elsie Silver

A False StartBuch (Taschenbuch)

16,90 €

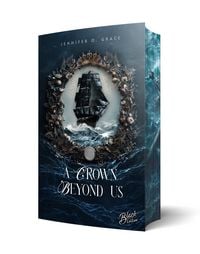

Jennifer O. Grace

A Crown beyond usBuch (Taschenbuch)

18,90 €

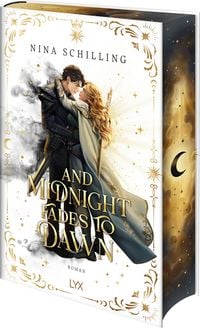

Nina Schilling

And Midnight Fades to DawnBuch (Gebundene Ausgabe)

24,00 €

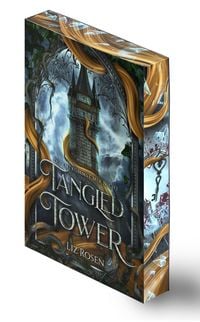

Liz Rosen

Tangled TowerBuch (Taschenbuch)

17,99 €

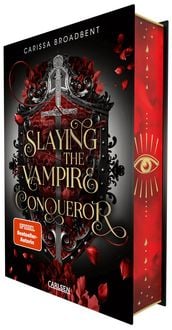

Carissa Broadbent

Slaying the Vampire Conqueror (Crowns of Nyaxia)Buch (Gebundene Ausgabe)

22,00 €

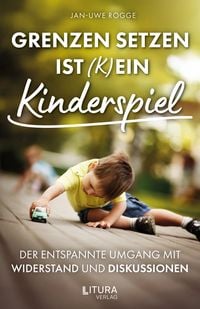

Jan Uwe Rogge

Grenzen setzen ist (k)ein KinderspielBuch (Taschenbuch)

17,99 €

Tanja Janz

Himmelsee – Wo der Wind von Liebe erzählt (Himmelsee 2)Buch (Taschenbuch)

13,00 €

Rebecca Yarros

Iron Flame – FlammengeküsstBuch (Taschenbuch)

16,00 €

Briar Boleyn

The Wings that Bind (Bloodwing Academy 3)Buch (Gebundene Ausgabe)

26,00 €

Petra Schier

Pfötchen, Strand und LiebesglückBuch (Taschenbuch)

13,00 €

Elif Shafak

Am Himmel die FlüsseBuch (Taschenbuch)

18,00 €

Anne Freytag

Laute NächteBuch (Gebundene Ausgabe)

24,00 €

Ewald Arenz

Ehrlich & SöhneBuch (Taschenbuch)

16,00 €

Daniel Mellem

Einstein im BadeBuch (Gebundene Ausgabe)

26,00 €

Francis Eden

The Lovely Side of DeathBuch (Taschenbuch)

18,00 €

Robert Seethaler

Der TrafikantBuch (Taschenbuch)

14,00 €

Anne Tyler

Drei Tage im JuniBuch (Taschenbuch)

16,00 €

Francesco Vidotto

Meine Berge bist duBuch (Gebundene Ausgabe)

24,00 €

Jessica Anthony

Es geht mir gutBuch (Taschenbuch)

14,00 €

Jane Austen

Stolz und VorurteilBuch (Gebundene Ausgabe)

9,00 €

Suzie Miller

Prima facieBuch (Taschenbuch)

16,00 €

Takis Würger

Der ClubBuch (Taschenbuch)

13,00 €

Jane Crilly

Der Gärtner von WimbledonBuch (Taschenbuch)

14,00 €

Cécile Tlili

Ein SommerabendBuch (Taschenbuch)

14,00 €

Gianrico Carofiglio

Der Horizont der NachtBuch (Gebundene Ausgabe)

25,00 €

Herbert Clyde Lewis

Gentleman über BordBuch (Taschenbuch)

14,00 €

Jane Campbell

Bei aller LiebeBuch (Taschenbuch)

14,00 €

Calla Henkel

Ein letztes GeschenkBuch (Taschenbuch)

18,00 €

Michael Connelly

Tote TageBuch (Taschenbuch)

23,90 €

Elif Shafak

Das Flüstern der FeigenbäumeBuch (Taschenbuch)

16,00 €

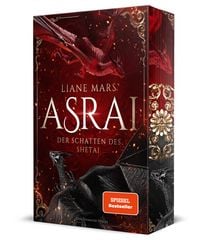

Liane Mars

Asrai - Der Schatten des ShetaiBuch (Taschenbuch)

20,00 €

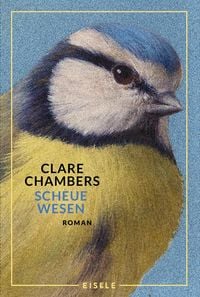

Clare Chambers

Scheue WesenBuch (Taschenbuch)

16,00 €

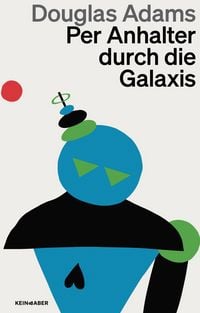

Douglas Adams

Per Anhalter durch die GalaxisBuch (Taschenbuch)

14,00 €

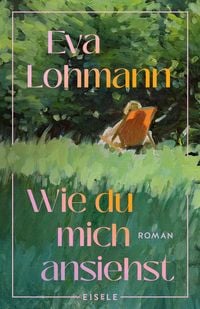

Eva Lohmann

Wie du mich ansiehstBuch (Taschenbuch)

15,00 €

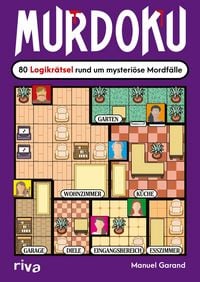

Manuel Garand

MurdokuBuch (Taschenbuch)

14,00 €

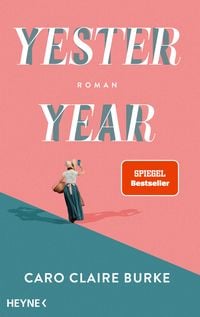

Caro Claire Burke

YesteryearBuch (Gebundene Ausgabe)

24,00 €

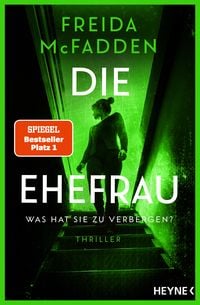

Freida McFadden

Die Ehefrau – Was hat sie zu verbergen?Buch (Taschenbuch)

17,00 €

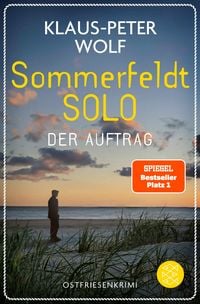

Klaus-Peter Wolf

Sommerfeldt Solo - Der AuftragBuch (Taschenbuch)

14,00 €

Caroline Seibt

Weil sie lügt (mit exklusivem Farbschnitt)Buch (Taschenbuch)

16,99 €

Jo Fischler

Klein aber totBuch (Taschenbuch)

14,00 €

Eva Almstädt

Akte Nordsee - Die letzte PredigtBuch (Taschenbuch)

13,99 €

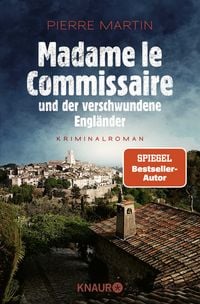

Pierre Martin

Madame le Commissaire und die tödliche RallyeBuch (Taschenbuch)

12,99 €

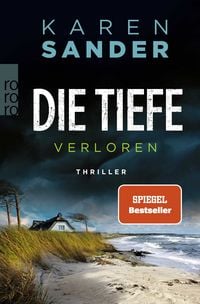

Karen Sander

Die Tiefe: VerlorenBuch (Taschenbuch)

14,00 €

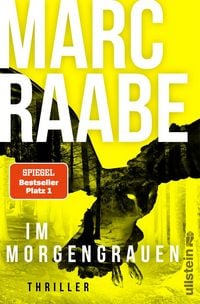

Marc Raabe

Im MorgengrauenBuch (Taschenbuch)

17,99 €

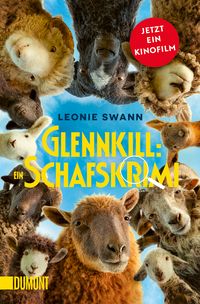

Leonie Swann

GlennkillBuch (Taschenbuch)

14,00 €

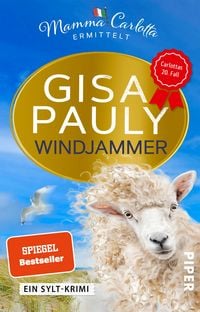

Gisa Pauly

WindjammerBuch (Taschenbuch)

13,00 €

**Gültig bis 24.06.2026 | Gültig für nicht preisgebundene Kalender und Schreibwaren | Einzelne Artikel können ausgeschlossen sein | Nicht kombinierbar mit anderen Gutscheinen oder Preisaktionen | Nur einmal pro Einkauf einlösbar | Gutschein wird auf max. 500€ Bestellwert angerechnet | Keine Barauszahlung | Nicht gültig für Versandkosten und Services

Bei bücher.de kannst du alle in Deutschland lieferbaren Bücher rund um die Uhr schnell und einfach bestellen. Sofern das von dir gewünschte Buch sofort lieferbar ist, erhältst du deine Ware oftmals schon am Folgetag, ansonsten innerhalb von 2-3 Werktagen. Natürlich kannst du deine Bücher per Rechnung, Lastschrift, Kreditkarte oder PayPal bezahlen. Dabei ist es egal, welche Bezahlart du wählst, es fallen keine zusätzlichen Kosten oder Gebühren für dich an.

Alle brauchen Bücher: Belletristik zur Unterhaltung, Fachbücher für Schule, Studium und Beruf, Ratgeber oder Sachbücher für Gesundheit & Ernährung, Haus & Hobby, Karriere, Finanzen, Lebensführung, Partnerschaft & Kindererziehung. Oder Reiseführer zur Vorbereitung und Begleitung bei der schönsten Zeit des Jahres, und und und, ... Bücher sind ein sehr altes Gut. In der Antike und im Mittelalter wurden Bücher noch von Hand geschrieben. Der klassische Buchdruck wurde dann im 15. Jahrhundert durch Johannes Gutenberg erfunden. Heute zählt der Börsenverein des Deutschen Buchhandels jedes Jahr knapp 90.000 Neuerscheinungen. Die meisten Novitäten entfallen dabei auf den Bereich Belletristik mit rund 14.000 Titeln, gefolgt von der deutschen Literatur mit 10.000 Büchern und dem Kinder- und Jugendbücher das mit 9.000 Titeln nur knapp dahinter liegt. Zweimal im Jahr stellen die Verlage ihre Neuerscheinungen vor: Im März auf der Leipziger Buchmesse sowie im Oktober auf der Frankfurter Buchmesse.

In Deutschland gibt es feste Preise für Bücher. Die Verlage sind laut Buchpreisbindungsgesetz (BuchPrG) verpflichtet, für jedes Buch einen festen Preis zu definieren, und jeder Händler ist verpflichtet, sich an diesen Preis zu halten. D.h. egal ob du auf dem Land oder in der Stadt, online oder im Laden dein gewünschtes Buch erwirbst, der Preis ist immer identisch und das schon seit 1888.

Bücher gelten in Deutschland als Kulturgut. Sie bilden den Spiegel einer Gesellschaft und archivieren den Geist und das Wissen einer Epoche. Ohne das gedruckte Wort gäbe es keinen Fortschritt und wissenschaftliche Erkenntnisse könnten nicht genauestens dokumentiert werden. Um das Kulturgut Buch zu schützen, wurde die Buchpreisbindung eingeführt und bis heute aufrechterhalten. Sinn und Zweck der Regelung ist zum einen der Erhalt eines breiten Buchangebots, denn wenn die Verlage unter Preisdruck geraten würden, könnten Bücher nicht mehr in der Vielfalt angeboten werden, wie wir sie heute vorfinden. Darüber hinaus könnten viele kleine Buchhandlungen sich nicht halten und somit wäre der Zugang zum Buch für manch einen erschwert.

Buch-Neuerscheinungen geben die Verlage in der Regel zunächst als Hardcover heraus. Unter Hardcover versteht man ein Buch mit festem Einband, das sehr robust in der Verarbeitung ist. Parallel zum Erscheinungstermin des Buches, wird i.d.R. das eBook verfügbar. Ca. ein Jahr später erscheint der Titel dann als Softcover, besser bekannt als Taschenbuch. Taschenbücher sind um einiges günstiger zu erwerben, allerdings erst einige Zeit später erhältlich und weniger strapazierfähig. Der durchschnittliche Preis eines Buches lag 2015 bei 14,59 EUR. Übrigens lesen 43% aller Leser nur gedruckte Bücher, wohingegen lediglich 2% ausschließlich eBooks lesen. 12% aller Leser nutzen Bücher und eBooks gleichermaßen und die übrigen Leser nutzen teilweile mehr gedruckte Bücher bzw. teilweise mehr eBooks.

Über 70% aller Buchleser lesen Bücher am liebsten auf dem Sofa. 57% lesen öfter im Bett und 52% suchen sich oft ein Plätzchen im Grünen zum Lesen. Eine Umfrage aus dem Jahr 2015 besagt, dass mehr als 9 Millionen Menschen täglich ein Buch in die Hand nehmen. Im Schnitt liest jeder Deutsche ein bis fünf Bücher pro Jahr. (Quelle: statista) Ganz egal, wo du am liebsten liest und wie viel: bücher.de ist dein Buchladen im Internet!